Filed Pursuant to Rule 497

Registration Statement No. 333-187447

PROSPECTUS SUPPLEMENT

(To prospectus dated June 6, 2014)

$100,000,000

6.25% Notes due 2024

We are an internally-managed, non-diversified closed-end management investment company that has elected to be regulated as a business development company under the Investment Company Act of 1940, as amended. Our investment objective is to maximize our portfolio total return by generating current income from our debt investments and capital appreciation from our equity-related investments.

We are offering $100,000,000 in aggregate principal amount of 6.25% notes due 2024, or the “Notes.” The Notes will mature on July 30, 2024. We will pay interest on the Notes on January 30, April 30, July 30 and October 30 of each year, beginning on July 30, 2014. We may redeem the Notes in whole or in part at any time or from time to time on or after July 30, 2017, at the redemption price set forth under “Specific Terms of the Notes and the Offering—Optional redemption” in this prospectus supplement. The Notes will be issued in minimum denominations of $25 and integral multiples of $25 in excess thereof.

The Notes will be our direct unsecured obligations and rank pari passu, or equally in right of payment, with all outstanding and future unsecured unsubordinated indebtedness issued by Hercules Technology Growth Capital, Inc.

We intend to list the Notes on the New York Stock Exchange, or NYSE, and we expect trading in the Notes on the NYSE to begin within 30 days of the original issue date under the symbol “HTGX.” The Notes are expected to trade “flat,” which means that purchasers will not pay, and sellers will not receive, any accrued and unpaid interest on the Notes that is not reflected in the trading price. Currently, there is no public market for the Notes.

An investment in the Notes involves risks that are described in the “Supplementary Risk Factors” section beginning on page S-16 in this prospectus supplement and the “Risk Factors” section beginning on page 11 of the accompanying prospectus.

This prospectus supplement and the accompanying prospectus contain important information you should know before investing in the Notes. Please read this prospectus supplement and the accompanying prospectus before investing and keep it for future reference. We file annual, quarterly and current reports, proxy statements and other information about us with the Securities and Exchange Commission. This information is available free of charge by contacting us at 400 Hamilton Avenue, Suite 310, Palo Alto, California 94301, or by telephone by calling collect at (650) 289-3060 or on our website at www.htgc.com. The information on the websites referred to herein is not incorporated by reference into this prospectus supplement or the accompanying prospectus. The SEC also maintains a website at www.sec.gov that contains information about us.

| Per Note | Total | |||||||

| Public offering price |

$ | 25.00 | $ | 100,000,000 | ||||

| Sales load (underwriting discounts and commissions) |

$ | 0.75 | $ | 3,000,000 | ||||

| Proceeds to us (before expenses)(1) |

$ | 24.25 | $ | 97,000,000 | ||||

| (1) | Before deducting expenses payable by us related to this offering, estimated at $500,000. |

The underwriters may also purchase up to an additional $4,600,000 total aggregate principal amount of Notes offered hereby, to cover overallotments, if any, within 30 days of the date of this prospectus supplement. If the underwriters exercise this option in full, the total public offering price will be $104,600,000, the total sales load (underwriting discounts and commissions) paid by us will be $3,138,000, and total proceeds, before expenses will be $101,462,000.

THE NOTES ARE NOT DEPOSITS OR OTHER OBLIGATIONS OF A BANK AND ARE NOT INSURED BY THE FEDERAL DEPOSIT INSURANCE CORPORATION OR ANY OTHER GOVERNMENT AGENCY.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus supplement or the accompanying prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Delivery of the Notes in book-entry form only through The Depository Trust Company will be made on or about July 14, 2014.

Joint Book-Running Managers

| Keefe, Bruyette & Woods A Stifel Company |

Jefferies | RBC Capital Markets |

Co-Managers

| BB&T Capital Markets | Janney Montgomery Scott | JMP Securities | Sterne Agee |

The date of this prospectus supplement is July 9, 2014.

You should rely only on the information contained in this prospectus supplement and the accompanying prospectus. We have not, and the underwriters have not, authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information contained in this prospectus supplement and the accompanying prospectus is accurate only as of the date on the front cover of this prospectus supplement or such prospectus, as applicable. Our business, financial condition, results of operations and prospects may have changed since that date.

Prospectus Supplement

Prospectus

SPECIFIC TERMS OF THE NOTES AND THE OFFERING

This prospectus supplement sets forth certain terms of the Notes that we are offering pursuant to this prospectus supplement and supplements the accompanying prospectus that is attached to the back of this prospectus supplement. This section outlines the specific legal and financial terms of the Notes. You should read this section together with the more general description of the Notes in the accompanying prospectus under the heading “Description of Our Debt Securities” before investing in the Notes. Capitalized terms used in this prospectus supplement and not otherwise defined shall have the meanings ascribed to them in the accompanying prospectus or in the indenture governing the Notes.

| Issuer |

Hercules Technology Growth Capital, Inc. |

| Title of the securities |

6.25% Notes due 2024 |

| Initial aggregate principal amount being offered |

$100,000,000 |

| Overallotment option |

The underwriters may also purchase from us up to an additional $4,600,000 aggregate principal amount of Notes to cover overallotments, if any, within 30 days of the date of this prospectus supplement. |

| Initial public offering price |

100% of the aggregate principal amount. |

| Principal payable at maturity |

100% of the aggregate principal amount; the principal amount of each Note will be payable on its stated maturity date at the office of the Trustee in The City of New York or at such other office designated by the Trustee. |

| Type of Note |

Fixed rate note |

| Listing |

We intend to list the Notes on the New York Stock Exchange within 30 days of the original issue date under the symbol “HTGX.” |

| Interest rate |

6.25% per year |

| Day count basis |

360-day year of twelve 30-day months |

| Original issue date |

July 14, 2014 |

| Stated maturity date |

July 30, 2024 |

| Date interest starts accruing |

July 14, 2014 |

| Interest payment dates |

Each January 30, April 30, July 30, and October 30, commencing July 30, 2014. If an interest payment date falls on a non-business day, the applicable interest payment will be made on the next business day and no additional interest will accrue as a result of such delayed payment. |

| Interest periods |

The initial interest period will be the period from and including July 14, 2014, to, but excluding, the initial interest payment date, and the subsequent interest periods will be the periods from and including an interest payment date to, but excluding, the next interest payment date or the stated maturity date, as the case may be. |

S-1

| Regular record dates for interest |

Each January 15, April 15, July 15 and October 15. |

| Specified currency |

U.S. Dollars |

| Place of payment |

New York City |

| Ranking of Notes |

The Notes will be our direct unsecured obligations and will rank: |

| • | pari passu with our other outstanding and future senior unsecured indebtedness, including without limitation, the $72.8 million 6.00% Convertible Senior Notes due 2016 (the “Convertible Senior Notes”); the approximately $84.5 million 7.00% Senior Notes due April 30, 2019 (the “April 2019 Notes”); the approximately $85.9 million 7.00% Senior Notes due September 30, 2019 (the “September 2019 Notes” and together with the April 2019 Notes, the “2019 Notes”) and the approximately $63.8 million fixed-rate asset-backed notes (the “Asset-Backed Notes”). |

| • | senior to any of our future indebtedness that expressly provides it is subordinated to the Notes. |

| • | effectively subordinated to all our existing and future secured indebtedness (including indebtedness that is initially unsecured to which we subsequently grant security), to the extent of the value of the assets securing such indebtedness, including without limitation, borrowings under our credit facilities. |

| • | structurally subordinated to all existing and future indebtedness and other obligations of any of our subsidiaries, including without limitation, the indebtedness of Hercules Technology II, L.P. and Hercules Technology III, L.P. and borrowings under our revolving senior secured credit facility with Wells Fargo Capital Finance (the “Wells Facility”). |

| Denominations |

We will issue the Notes in denominations of $25 and integral multiples of $25 in excess thereof. |

| Business day |

Each Monday, Tuesday, Wednesday, Thursday and Friday that is not a day on which banking institutions in New York City are authorized or required by law or executive order to close. |

| Optional redemption |

The Notes may be redeemed in whole or in part at any time or from time to time at our option on or after July 30, 2017, upon not less than 30 days nor more than 60 days written notice by mail prior to the date fixed for redemption thereof, at a redemption price of 100% of the outstanding principal amount thereof plus accrued and unpaid interest payments otherwise payable for the then-current quarterly interest period accrued to but not including the date fixed for redemption. |

| You may be prevented from exchanging or transferring the Notes when they are subject to redemption. In case any Notes |

S-2

| are to be redeemed in part only, the redemption notice will provide that, upon surrender of such Note, you will receive, without a charge, a new Note or Notes of authorized denominations representing the principal amount of your remaining unredeemed Notes. Any exercise of our option to redeem the Notes will be done in compliance with the indenture and the Investment Company Act of 1940, as amended, and the rules, regulations and interpretations promulgated thereunder, which we collectively refer to as the 1940 Act, to the extent applicable. |

| If we redeem only some of the Notes, the Trustee or DTC, as applicable, will determine the method for selection of the particular Notes to be redeemed, in accordance with the indenture and the 1940 Act and in accordance with the rules of any national securities exchange or quotation system on which the Notes are listed, in each case, to the extent applicable. Unless we default in payment of the redemption price, on and after the date of redemption, interest will cease to accrue on the Notes called for redemption. |

| Under our credit facility with Union Bank, N.A. (the “Union Bank Facility”), as currently in effect, and to the extent still in effect at the time our optional redemption right matures, we would not be permitted to exercise that right without the consent of the lenders. |

| Sinking fund |

The Notes will not be subject to any sinking fund. |

| Repayment at option of Holders |

Holders will not have the option to have the Notes repaid prior to the stated maturity date. |

| Defeasance and covenant defeasance |

The Notes are subject to defeasance by us. |

| The Notes are subject to covenant defeasance by us. |

| Under the Union Bank Facility, as currently in effect, we would be prohibited from defeasing the Notes or effecting covenant defeasance under the Notes without the consent of the lenders. |

| Form of Notes |

The Notes will be represented by global securities that will be deposited and registered in the name of The Depository Trust Company, or DTC, or its nominee. Except in limited circumstances, you will not receive certificates for the Notes. Beneficial interests in the Notes will be represented through book-entry accounts of financial institutions acting on behalf of beneficial owners as direct and indirect participants in DTC. Investors may elect to hold interests in the Notes through either DTC, if they are a participant, or indirectly through organizations which are participants in DTC. |

S-3

| Trustee, Paying Agent and Security Registrar |

U.S. Bank National Association |

| Other covenants |

In addition to the covenants described in the prospectus attached to this prospectus supplement, the following covenants shall apply to the Notes: |

| • | We agree that for the period of time during which the Notes are outstanding, we will not violate Section 18(a)(1)(A) as modified by Section 61(a)(1) of the 1940 Act or any successor provisions, whether or not we continue to be subject to such provisions of the 1940 Act, but giving effect, in either case, to any exemptive relief granted to us by the U.S. Securities and Exchange Commission (the “SEC”). These provisions generally prohibit us from making additional borrowings, including through the issuance of additional debt or the sale of additional debt securities, unless our asset coverage, as defined in the 1940 Act, equals at least 200% after such borrowings. |

| • | We agree that for the period of time during which the Notes are outstanding, we will not violate Section 18(a)(1)(B) as modified by Section 61(a)(1) of the 1940 Act or any successor provisions, giving effect to (i) any exemptive relief granted to us by the SEC and (ii) no-action relief granted by the SEC to another business development company (“BDC”) (or to us if we determine to seek such similar no-action or other relief) permitting the BDC to declare any cash dividend or distribution notwithstanding the prohibition contained in Section 18(a)(1)(B) as modified by Section 61(a)(1) of the 1940 Act in order to maintain the BDC’s status as a regulated investment company under Subchapter M of the Internal Revenue Code of 1986. These provisions generally prohibit us from declaring any cash dividend or distribution upon any class of our capital stock, or purchasing any such capital stock if our asset coverage, as defined in the 1940 Act, is below 200% at the time of the declaration of the dividend or distribution or the purchase and after deducting the amount of such dividend, distribution or purchase. |

| Reports by the Company |

If, at any time, we are not subject to the reporting requirements of Sections 13 or 15(d) of the Securities Exchange Act of 1934 to file any periodic reports with the SEC, we agree to furnish to holders of the Notes and the Trustee, for the period of time during which the Notes are outstanding, our audited annual consolidated financial statements, within 90 days of our fiscal year end, and unaudited interim consolidated financial statements, within 45 days of our fiscal quarter end (other than our fourth fiscal |

S-4

| quarter). All such financial statements will be prepared, in all material respects, in accordance with applicable United States generally accepted accounting principles. |

| Modifications to events of default |

The following events of default, as described in the prospectus attached to this prospectus supplement: |

| • | We do not pay the principal of, or any premium on, a debt security of the series on its due date, and do not cure this default within 5 days. |

| • | On the last business day of each of 24 consecutive calendar months, we have an asset coverage of less than 100%. |

| with respect to the Notes has been revised to read as follows: |

| • | We do not pay the principal of, or any premium on, any Note on its due date. |

| • | On the last business day of each of 24 consecutive calendar months, we have an asset coverage of less than 100%, giving effect to any exemptive relief granted to us by the SEC. |

| Global Clearance and Settlement Procedures |

Interests in the Notes will trade in DTC’s Same Day Funds Settlement System, and any permitted secondary market trading activity in such Notes will, therefore, be required by DTC to be settled in immediately available funds. None of the issuer, the Trustee or the paying agent will have any responsibility for the performance by DTC or its participants or indirect participants of their respective obligations under the rules and procedures governing their operations. |

| Use of Proceeds |

We estimate that the net proceeds we receive from the sale of the $100.0 million aggregate principal amount of Notes in this offering will be approximately $96.5 million (or approximately $101.4 million if the underwriters fully exercise their overallotment option) after deducting the underwriting discount of approximately $3.0 million (or approximately $3.2 million if the underwriters fully exercise their overallotment option) payable by us and estimated offering expenses of approximately $500,000 payable by us. We expect to use the net proceeds from this offering to fund investments in debt and equity securities in accordance with our investment objective and for other general corporate purposes. We may also use the net proceeds from this offering to fund the conversion of any of our Convertible Senior Notes which holders may elect to convert. |

S-5

The matters discussed in this prospectus supplement and the accompanying prospectus, as well as in future oral and written statements by management of Hercules Technology Growth Capital, that are forward-looking statements are based on current management expectations that involve substantial risks and uncertainties which could cause actual results to differ materially from the results expressed in, or implied by, these forward-looking statements. Forward-looking statements relate to future events or our future financial performance. We generally identify forward-looking statements by terminology such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “could,” “intends,” “target,” “projects,” “contemplates,” “believes,” “estimates,” “predicts,” “potential” or “continue” or the negative of these terms or other similar words. Important assumptions include our ability to originate new investments, achieve certain margins and levels of profitability, the availability of additional capital, and the ability to maintain certain debt to asset ratios. In light of these and other uncertainties, the inclusion of a projection or forward-looking statement in this prospectus should not be regarded as a representation by us that our plans or objectives will be achieved. The forward-looking statements contained in this prospectus supplement and the accompanying prospectus include statements as to:

| • | our future operating results; |

| • | our business prospects and the prospects of our prospective portfolio companies; |

| • | the impact of investments that we expect to make; |

| • | the impact of a protracted decline in the liquidity of credit markets on our business; |

| • | our informal relationships with third parties including in the venture capital industry; |

| • | the expected market for venture capital investments and our addressable market; |

| • | the dependence of our future success on the general economy and its impact on the industries in which we invest; |

| • | our ability to access debt markets and equity markets; |

| • | the ability of our portfolio companies to achieve their objectives; |

| • | our expected financings and investments; |

| • | our regulatory structure and tax status; |

| • | our ability to operate as a business development company, a small business investment company and a regulated investment company, or RIC; |

| • | the adequacy of our cash resources and working capital; |

| • | the timing of cash flows, if any, from the operations of our portfolio companies; |

| • | the timing, form and amount of any dividend distributions; |

| • | the impact of fluctuations in interest rates on our business; |

| • | the valuation of any investments in portfolio companies, particularly those having no liquid trading market; and |

| • | our ability to recover unrealized losses. |

For a discussion of factors that could cause our actual results to differ from forward-looking statements contained in this prospectus supplement and the accompanying prospectus, please see the discussion under “Supplementary Risk Factors” in this prospectus supplement and “Risk Factors” in the accompanying prospectus.

S-6

You should not place undue reliance on these forward-looking statements. The forward-looking statements made in this prospectus relate only to events as of the date on which the statements are made and are excluded from the safe harbor protection provided by Section 27A of the Securities Act of 1933.

Industry and Market Data

We have compiled certain industry estimates presented in this prospectus supplement and the accompanying prospectus from internally generated information and data. While we believe our estimates are reliable, they have not been verified by any independent sources. The estimates are based on a number of assumptions, including increasing investment in venture capital and private equity-backed companies. Actual results may differ from projections and estimates, and this market may not grow at the rates projected, or at all. If this market fails to grow at projected rates, our business and the market price of our securities, including the Notes, could be materially adversely affected.

S-7

This summary highlights some of the information in this prospectus supplement and may not contain all of the information that is important to you. For a more complete understanding of this offering, we encourage you to read this entire prospectus supplement and the accompanying prospectus and the documents that are referenced in this prospectus supplement and the accompanying prospectus, together with any accompanying supplements. In this prospectus supplement and the accompanying prospectus, unless the context otherwise requires, the “Company,” “Hercules Technology Growth Capital,” “Hercules,” “we,” “us” and “our” refer to Hercules Technology Growth Capital, Inc. and our wholly-owned subsidiaries.

Our Company

We are a specialty finance company focused on providing senior secured loans to venture capital-backed companies in technology-related markets, including technology, biotechnology, life science and energy and renewables technology industries at all stages of development. Our investment objective is to maximize our portfolio total return by generating current income from our debt investments and capital appreciation from our equity-related investments. We are an internally-managed, non-diversified closed-end investment company that has elected to be regulated as a business development company under the Investment Company Act of 1940, or the 1940 Act.

As of March 31, 2014, our total assets were approximately $1.2 billion, of which our investments comprised $890.7 million at fair value and $887.6 million at cost. Since inception through March 31, 2014, we have made debt and equity commitments of approximately $4.2 billion to our portfolio companies.

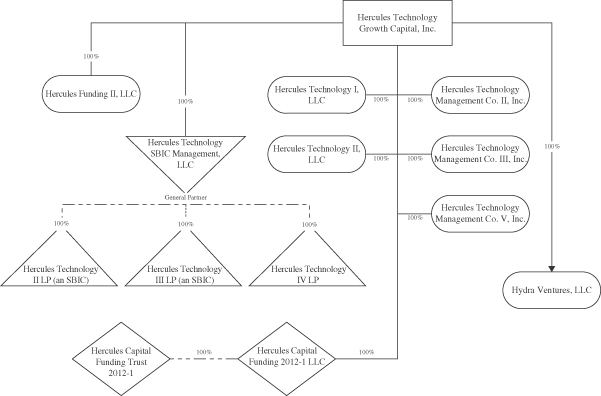

We also make investments in qualifying small businesses through two wholly-owned, small business investment company, or SBIC, subsidiaries, Hercules Technology II, L.P., or HT II, and Hercules Technology III, L.P., or HT III. HT II and HT III hold approximately $143.7 million and $290.0 million in assets, respectively, and accounted for approximately 9.5% and 19.3% of our total assets, respectively, prior to consolidation at March 31, 2014. As of March 31, 2014, the maximum statutory limit on the dollar amount of combined outstanding SBA guaranteed debentures is $225.0 million, subject to periodic adjustments by the SBA. In aggregate, at March 31, 2014, with our net investment of $112.5 million, HT II and HT III have the capacity to issue a total of $225.0 million of SBA-guaranteed debentures, subject to SBA approval. In March 2014, we repaid $34.8 million of SBA debentures under HT II, priced at approximately 6.38%, including annual fees. At March 31, 2014, we have issued $190.2 million in SBA-guaranteed debentures in our SBIC subsidiaries. See “Regulation—Small Business Administration Regulations” in the accompanying prospectus for additional information regarding our SBIC subsidiaries.

Our portfolio is comprised of, and we anticipate that our portfolio will continue to be comprised of, investments in technology-related companies at various stages of development. Consistent with regulatory requirements, we invest primarily in United States based companies and, to a lesser extent, in foreign companies. See “Regulation—Qualifying Assets.” As of March 31, 2014, our proprietary structured query language-based (SQL) database system included over 35,300 technology-related companies and approximately 8,900 venture capital, private equity sponsors/investors, as well as various other industry contacts. Our principal executive office is located in Palo Alto, CA, and we have additional offices in Boston, MA, New York, NY and McLean, VA.

Our goal is to be the leading structured debt financing provider of choice for venture capital backed companies in technology-related markets requiring sophisticated and customized financing solutions. Our strategy is to evaluate and invest in a broad range of companies in technology-related markets, including, technology, biotechnology, life science, and energy and renewables technology companies and to offer a full

S-8

suite of growth capital products up and down the capital structure. We invest primarily in private companies and, to a lesser extent, public companies. We invest primarily in structured debt with warrants and, to a lesser extent, in senior debt and equity investments. We use the term “structured debt with warrants” to refer to any debt investment, such as a senior or subordinated secured loan, that is coupled with an equity component, including warrants, options or rights to purchase common or preferred stock. Our structured debt with warrants investments will typically be secured by select or all of the assets of the portfolio company.

We focus our investments in companies active in technology industry sub-sectors characterized by products or services that require advanced technologies, including, but not limited to, computer software and hardware, networking systems, semiconductors, semiconductor capital equipment, information technology infrastructure or services, internet consumer and business services, telecommunications, telecommunications equipment, renewable or alternative energy, media and life science. Within the life science sub-sector, we generally focus on medical devices, bio-pharmaceutical, drug discovery, drug delivery, health care services and information systems companies. Within the energy technology sub-sector, we focus on sustainable and renewable energy technologies and energy efficiency and monitoring technologies. We refer to all of these companies as “technology-related” companies and intend, under normal circumstances, to invest at least 80% of the value of our total assets in such businesses.

Our investment objective is to maximize our portfolio total return by generating current income from our debt investments and capital appreciation from our equity-related investments. Our primary business objectives are to increase our net income, net operating income and net asset value by investing in structured debt with warrants and equity of venture capital-backed companies in technology-related markets with attractive current yields and the potential for equity appreciation and realized gains. Our structured debt investments typically include warrants or other equity interests. Our equity ownership in our portfolio companies may exceed 25% of the voting securities of such companies, which represents a controlling interest under the 1940 Act. In some cases, we receive the right to make additional equity investments in our portfolio companies in connection with future equity financing rounds. Capital that we provide directly to venture capital-backed companies in technology-related markets is generally used for growth and general working capital purposes as well as in select cases for acquisitions or recapitalizations.

We are prohibited from co-investing with our affiliates, such as Hercules Energy Technology and Resource Management, Inc., or Hercules Energy Technology, and its affiliates, absent the receipt of exemptive relief from the SEC. However, we, Hercules Energy Technology and its affiliates have filed an exemptive application with the SEC to permit greater flexibility to negotiate the terms of co-investments with Hercules Energy Technology and its affiliates in a manner consistent with our investment objective, positions, policies, strategies and restrictions as well as regulatory requirements and other pertinent factors. This exemptive application is still pending, and there can be no assurance that we will receive exemptive relief from the SEC to permit us to co-invest with Hercules Energy Technology and its affiliates. Under the terms of such relief permitting us to co-invest with Hercules Energy Technology and its affiliates, a “required majority” (as defined in Section 57(o) of the 1940 Act) of our independent directors must make certain conclusions in connection with a co-investment transaction, including that (1) the terms of the transaction, including the consideration to be paid, are reasonable and fair to us and our stockholders and do not involve overreaching of us or our stockholders on the part of any person concerned and (2) the transaction is consistent with the interests of our shareholders and is consistent with our investment objective and strategies. We may continue to make investments in energy and renewables technology companies under certain conditions, such as opportunities predating the funding of Hercules Energy Technology, investments in our existing portfolio companies, including follow on investments, or other specific circumstances. We, in general, will not focus on making energy and renewables technology investments subsequent to the funding of Hercules Energy Technology.

As of March 31, 2014, our investment professionals, including Manuel A. Henriquez, our co-founder, Chairman, President and Chief Executive Officer, are currently comprised of 38 professionals who

S-9

have, on average, more than 15 years of experience in venture capital, structured finance, commercial lending or acquisition finance with the types of technology-related companies that we are targeting. We believe that we can leverage the experience and relationships of our management team to successfully identify attractive investment opportunities, underwrite prospective portfolio companies and structure customized financing solutions.

Our Market Opportunity

We believe that technology-related companies compete in one of the largest and most rapidly growing sectors of the U.S. economy and that continued growth is supported by ongoing innovation and performance improvements in technology products as well as the adoption of technology across virtually all industries in response to competitive pressures. We believe that an attractive market opportunity exists for a specialty finance company focused primarily on investments in structured debt with warrants in technology-related companies for the following reasons:

| • | Technology-related companies have generally been underserved by traditional lending sources; |

| • | Unfulfilled demand exists for structured debt financing to technology-related companies as the number of lenders has declined due to the recent financial market turmoil; and |

| • | Structured debt with warrants products are less dilutive and complement equity financing from venture capital and private equity funds. |

Technology-Related Companies are Underserved by Traditional Lenders. We believe many viable technology-related companies backed by financial sponsors have been unable to obtain sufficient growth financing from traditional lenders, including financial services companies such as commercial banks and finance companies, because traditional lenders have continued to consolidate and have adopted a more risk-averse approach to lending. More importantly, we believe traditional lenders are typically unable to underwrite the risk associated with these companies effectively.

S-10

The unique cash flow characteristics of many technology-related companies, which typically include significant research and development expenditures and high projected revenue growth thus often making such companies difficult to evaluate from a credit perspective. In addition, the balance sheets of these companies often include a disproportionately large amount of intellectual property assets, which can be difficult to value. Finally, the speed of innovation in technology and rapid shifts in consumer demand and market share add to the difficulty in evaluating technology-related companies.

Due to the difficulties described above, we believe traditional lenders are generally refraining from entering the structured debt financing marketplace, instead preferring the risk-reward profile of asset based lending. Traditional lenders generally do not have flexible product offerings that meet the needs of technology-related companies. The financing products offered by traditional lenders typically impose on borrowers many restrictive covenants and conditions, including limiting cash outflows and requiring a significant depository relationship to facilitate rapid liquidation.

Unfulfilled Demand for Structured Debt Financing to Technology-Related Companies. Private debt capital in the form of structured debt financing from specialty finance companies continues to be an important source of funding for technology-related companies. We believe that the level of demand for structured debt financing is a function of the level of annual venture equity investment activity.

We believe that demand for structured debt financing is currently underserved. The venture capital market for the technology-related companies in which we invest has been active and is continuing to show signs of increased investment activity. Therefore, to the extent we have capital available, we believe this is an opportune time to be active in the structured lending market for technology-related companies.

Structured Debt with Warrants Products Complement Equity Financing From Venture Capital and Private Equity Funds. We believe that technology-related companies and their financial sponsors will continue to view structured debt securities as an attractive source of capital because it augments the capital provided by venture capital and private equity funds. We believe that our structured debt with warrants product provides access to growth capital that otherwise may only be available through incremental investments by existing equity investors. As such, we provide portfolio companies and their financial sponsors with an opportunity to diversify their capital sources. Generally, we believe technology-related companies at all stages of development target a portion of their capital to be debt in an attempt to achieve a higher valuation through internal growth. In addition, because financial sponsor-backed companies have reached a more mature stage prior to reaching a liquidity event, we believe our investments could provide the debt capital needed to grow or recapitalize during the extended period prior to liquidity events.

Our Business Strategy

Our strategy to achieve our investment objective includes the following key elements:

Leverage the Experience and Industry Relationships of Our Management Team and Investment Professionals. We have assembled a team of experienced investment professionals with extensive experience as venture capitalists, commercial lenders, and originators of structured debt and equity investments in technology-related companies.

Mitigate Risk of Principal Loss and Build a Portfolio of Equity-Related Securities. We expect that our investments have the potential to produce attractive risk adjusted returns through current income, in the form of interest and fee income, as well as capital appreciation from equity-related securities. We seek to mitigate the risk of loss on our debt investments through the combination of loan principal amortization, cash interest payments, relatively short maturities (generally 12-60 months), security interests in the assets of our portfolio

S-11

companies, and on select investment covenants requiring prospective portfolio companies to have certain amounts of available cash at the time of our investment and the continued support from a venture capital or private equity firm at the time we make our investment.

Provide Customized Financing Complementary to Financial Sponsors’ Capital. We offer a broad range of investment structures and possess expertise and experience to effectively structure and price investments in technology-related companies.

Invest at Various Stages of Development. We provide growth capital to technology-related companies at all stages of development, including select publicly listed companies, select special opportunity lower middle market companies that require additional capital to fund acquisitions, recapitalizations and refinancing and established-stage companies.

Benefit from Our Efficient Organizational Structure. We believe that our corporate structure enables us to be a long-term partner for our portfolio companies in contrast to traditional investment funds, which typically have a limited life. In addition, because of our access to the equity markets, we believe that we may benefit from a lower cost of capital than that available to private investment funds.

Deal Sourcing Through Our Proprietary Database. We have developed a proprietary and comprehensive SQL database system to track various aspects of our investment process including sourcing, originations, transaction monitoring and post-investment performance.

Recent Developments

ATM Program Update

During the period from June 1, 2014 to June 30, 2014 (with settlement through July 1, 2014), we sold 650,000 shares of our common stock at an average price of $15.6495 per share, and raised $10.2 million gross proceeds, under our at-the-market offering program, or ATM Program. Net proceeds were $10.0 million after commissions to the broker-dealer on shares sold and offering costs.

Appointment of Chief Operating Officer

Effective July 8, 2014, the Company’s Board of Directors appointed Harry A. Feuerstein as the Company’s Chief Operating Officer. Mr. Feuerstein, age 52, joined the Company in July 2014. Mr. Feuerstein previously served as president and as a board member of Merryck & Co., Americas, and also served as an Operating Executive of Morgan Joseph Tri Artisan and as a Managing Director of W2 GreenTech. Prior to such roles, Mr. Feuerstein held several executive-level positions at Siemens USA, including as CEO of Siemens Government Inc., with experience in energy, technology and healthcare matters. Mr. Feuerstein is also the former CEO of a subsidiary of Trizechahn Corporation and was a partner at National Capital Companies and its related broker dealer. Mr. Feuerstein received his BA from Washington and Lee University, and he received an MBA from Hofstra University.

Appointment of Director

On July 8, 2014, our Board of Directors elected Mr. Thomas Fallon as a director of the Company. In connection with his election, the Board of Directors increased the size of the Board of Directors to four directors. There are no arrangements or understandings between Mr. Fallon and any other persons pursuant to which Mr. Fallon was elected as a director of the Company. Mr. Fallon will be entitled to applicable retainer and meeting fees and an option award pursuant to the Company’s director compensation arrangements, under terms consistent with those previously disclosed by the Company. Mr. Fallon also will be entitled to enter into an indemnification agreement with the Company.

S-12

Mr. Fallon joined the Company as a Director in 2014 and will hold office for a term expiring in 2015. Mr. Fallon has served as Chief Executive Officer of Infinera Corporation since June 2013 and as a member of Infinera’s board of directors since July 2009. From January 2010 to June 2013, Mr. Fallon served as Infinera’s President and Chief Executive Officer, and Mr. Fallon served as Infinera’s Chief Operating Officer from October 2006 to December 2009, and as its Vice President of Engineering and Operations from April 2004 to September 2006. From August 2003 to March 2004, Mr. Fallon was Vice President, Corporate Quality and Development Operations of Cisco Systems, Inc., a networking and telecommunications company. From May 2001 to August 2003, Mr. Fallon served as General Manager of Cisco Systems’ Optical Transport Business Unit. Mr. Fallon holds a B.S.M.E. and M.B.A. from the University of Texas at Austin, and is currently a member of the Engineering Advisory Board of the University of Texas at Austin.

Amendment to Union Bank Facility

On July 8, 2014, the Company entered into an amendment to the Union Bank Facility. Pursuant to the terms of the amendment, the Company is permitted to increase its unsecured indebtedness by an aggregate original principal amount not to exceed $275 million incurred after March 30, 2012 in one or more issuances, provided certain conditions are satisfied for each issuance.

Convertible Senior Notes

In April 2011, we issued $75.0 million in aggregate principal amount of 6.00% convertible senior notes, or the Convertible Senior Notes, due 2016. As of June 30, 2014, the carrying value of the Convertible Senior Notes, comprised of the aggregate principal amount outstanding less the unaccreted discount initially recorded upon issuance of the Convertible Senior Notes, is approximately $73.1 million.

The Convertible Senior Notes are convertible into shares of our common stock beginning October 15, 2015, or, under certain circumstances, earlier. Upon conversion of the Convertible Notes, we have the choice to pay or deliver, as the case may be, at our election, cash, shares of our common stock or a combination of cash and shares of our common stock. The current conversion price of the Convertible Senior Notes is approximately $11.49 per share of common stock, in each case subject to adjustment in certain circumstances. Upon meeting the stock trading price conversion requirement during the three months ended June 30, 2014, the Convertible Senior Notes became convertible on July 1, 2014 and continue to be convertible through September 30, 2014.

Portfolio Activity for Quarter Ended June 30, 2014

New Originations

During the quarter ended June 30, 2014, Hercules has originated approximately $238.6 million of debt commitments to new and existing portfolio companies.

Commitments

During the quarter ended June 30, 2014, Hercules made new commitments to the following thirteen companies, assisting in their future growth and development:

| • | $35.0 million commitment to Alimera Sciences, Inc., a biopharmaceutical company that specializes in the research, development and commercialization of prescription ophthalmic pharmaceuticals. |

| • | $30.0 million commitment to Nanotherapeutics, Inc., an integrated biopharmaceutical company with a major focus on developing a diversified proprietary pipeline of products having both biodefense and medical applications. |

S-13

| • | $25.5 million commitment to CareCloud Corporation, a provider of cloud-based practice management, electronic health record, and medical billing software and services. |

| • | $22.5 million commitment to SkyCross, Inc., a global designer and manufacturer of advanced antenna and RF solutions. |

| • | $20.0 million commitment to a biomaterial company that manufactures and sells a broad range of medical devices. |

| • | $15.0 million commitment to Celator Pharmaceuticals, Inc., a pharmaceutical company developing advanced therapies to treat cancer based identifying synergistic ratios of drugs that improve tumor cell kill. |

| • | $15.0 million commitment to a software company that provides a commerce platform for retailers. |

| • | $10.0 million commitment to Pong Research Corporation, which develops cases for the Apple iPhone, iPad, and Android smartphones to increase range and transmit stronger signal, while reducing exposure to wireless energy. |

| • | $10.0 million commitment to Quanterix Corporation, a leader in high definition diagnostics, including its Simoa platform which uses single molecule measurements to access previously undetectable proteins. |

| • | $10.0 million commitment to a specialty biopharmaceutical company focused on the development, manufacturing and commercialization of products for aesthetic medicine |

| • | $10.0 million commitment to a company that develops specialty contact lenses. |

| • | $4.5 million commitment to Poplicus, Inc., a software company that creates proprietary analytics from big data in the public sector. |

| • | $4.0 million commitment to Zosano Pharma, Inc., a biopharmaceutical company developing a transdermal delivery technology for a broad range of therapeutic indications. |

In addition, Hercules provided approximately $27.1 million of debt commitments and renewals to existing portfolio companies during the quarter ended June 30, 2014.

It is important to note that certain commitments may expire without being drawn upon, and commitments do not necessarily represent future cash requirements or future earning assets for Hercules. Our commitments may include conditions, such as reaching certain milestones, before the Hercules debt commitment would become available. Hercules is instituting more funding or performance based milestone requirements to mitigate risk which will affect our actual funding levels.

Principal Repayments

During the quarter ended June 30, 2014, Hercules received approximately $68.1 million in principal repayments, of which approximately $38.7 million were unscheduled early repayments.

Portfolio Company Liquidity Events

In April 2014, Hercules portfolio company Glori Energy, Inc. (NASDAQ: GLRI) completed its $185 million reverse merger with Infinity Cross Border Acquisition Corp. (NASDAQ: INXB) and closed a share tender offer and a warrant tender offer.

S-14

Current Companies in IPO Registration:

During the quarter ended June 30, 2014, Hercules had warrant and equity positions in five (5) portfolio companies that had filed Registration Statements in contemplation of a potential IPO:

| • | Box, Inc. |

| • | Dance Biopharm, Inc. |

| • | Good Technology |

| • | Zosano Pharma, Inc. |

| • | One company filed confidentially under the Jobs Act |

There can be no assurances that these companies will complete their IPOs in a timely manner or at all.

Corporate Information

Our principal executive offices are located at 400 Hamilton Avenue, Suite 310, Palo Alto, California 94301, and our telephone number is (650) 289-3060. We also have offices in Boston, Massachusetts, New York, New York and McLean, Virginia. We maintain a website on the Internet at www.htgc.com. Information contained in our website is not incorporated by reference into this prospectus supplement or the accompanying prospectus, and you should not consider that information to be part of this prospectus.

S-15

Investing in our securities involves a number of significant risks. Before you invest in our securities, you should be aware of various risks, including those described below and those set forth in the accompanying prospectus. You should carefully consider these risk factors, together with all of the other information included in this prospectus supplement and the accompanying prospectus, before you decide whether to make an investment in our securities. The risks set out below and in the accompanying prospectus are not the only risks we face. Additional risks and uncertainties not presently known to us or not presently deemed material by us may also impair our operations and performance. If any of the following events occur, our business, financial condition, results of operations and cash flows could be materially and adversely affected which could materially adversely affect our ability to repay principal and interest on the Notes. In addition, the market price of the Notes and our net asset value could decline, and you may lose all or part of your investment. The risk factors described below, together with those set forth in the accompanying prospectus, are the principal risk factors associated with an investment in our securities, including the Notes, as well as those factors generally associated with an investment company with investment objectives, investment policies, capital structure or trading markets similar to ours.

The Notes will be unsecured and therefore will be effectively subordinated to any secured indebtedness we have currently incurred or may incur in the future.

The Notes will not be secured by any of our assets or any of the assets of our subsidiaries. As a result, the Notes are effectively subordinated to any secured indebtedness we or our subsidiaries have currently incurred and may incur in the future (or any indebtedness that is initially unsecured to which we subsequently grant security) to the extent of the value of the assets securing such indebtedness. In any liquidation, dissolution, bankruptcy or other similar proceeding, the holders of any of our existing or future secured indebtedness and the secured indebtedness of our subsidiaries may assert rights against the assets pledged to secure that indebtedness in order to receive full payment of their indebtedness before the assets may be used to pay other creditors, including the holders of the Notes. As of March 31, 2014, we had no borrowings outstanding under our Union Bank Facility, which is secured by debt investments in our portfolio companies and related assets or our Wells Facility, which is secured by loans in the borrowing base for the Wells Facility.

The Notes will be structurally subordinated to the indebtedness and other liabilities of our subsidiaries.

The Notes are obligations exclusively of Hercules Technology Growth Capital, Inc. and not of any of our subsidiaries. None of our subsidiaries is a guarantor of the Notes and the Notes are not required to be guaranteed by any subsidiaries we may acquire or create in the future. A significant portion of the indebtedness required to be consolidated on our balance sheet is held through our SBIC subsidiaries. For example, at March 31, 2014, we have issued $190.2 million in SBA-guaranteed debentures in our SBIC subsidiaries. The assets of such subsidiaries are not directly available to satisfy the claims of our creditors, including holders of the Notes. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Financial Condition, Liquidity and Capital Resources” in the accompanying prospectus for more detail on the SBA-guaranteed debentures.

Except to the extent we are a creditor with recognized claims against our subsidiaries, all claims of creditors (including trade creditors) and holders of preferred stock, if any, of our subsidiaries will have priority over our equity interests in such subsidiaries (and therefore the claims of our creditors, including holders of the Notes) with respect to the assets of such subsidiaries. Even if we are recognized as a creditor of one or more of our subsidiaries, our claims would still be effectively subordinated to any security interests in the assets of any such subsidiary and to any indebtedness or other liabilities of any such subsidiary senior to our claims. Consequently, the Notes will be structurally subordinated to all indebtedness and other liabilities (including trade payables) of any of our subsidiaries and any subsidiaries that we may in the future acquire or establish as financing vehicles or otherwise. As of March 31, 2014, we had no borrowings outstanding under either our Wells Facility or our Union

S-16

Bank Facility and approximately $190.2 million of indebtedness outstanding incurred by our SBIC subsidiaries, HT II and HT III. All of such indebtedness would be structurally senior to the Notes. In addition, our subsidiaries may incur substantial additional indebtedness in the future, all of which would be structurally senior to the Notes.

The indenture under which the Notes will be issued will contain limited protection for holders of the Notes.

The indenture under which the Notes will be issued offers limited protection to holders of the Notes. The terms of the indenture and the Notes do not restrict our or any of our subsidiaries’ ability to engage in, or otherwise be a party to, a variety of corporate transactions, circumstances or events that could have an adverse impact on your investment in the Notes. In particular, the terms of the indenture and the Notes will not place any restrictions on our or our subsidiaries’ ability to:

| • | issue securities or otherwise incur additional indebtedness or other obligations, including (1) any indebtedness or other obligations that would be equal in right of payment to the Notes, (2) any indebtedness or other obligations that would be secured and therefore rank effectively senior in right of payment to the Notes to the extent of the values of the assets securing such debt, (3) indebtedness of ours that is guaranteed by one or more of our subsidiaries and which therefore is structurally senior to the Notes and (4) securities, indebtedness or obligations issued or incurred by our subsidiaries that would be senior to our equity interests in our subsidiaries and therefore rank structurally senior to the Notes with respect to the assets of our subsidiaries, in each case other than an incurrence of indebtedness or other obligation that would cause a violation of Section 18(a)(1)(A) as modified by Section 61(a)(1) of the 1940 Act or any successor provisions, whether or not we continue to be subject to such provisions of the 1940 Act, but giving effect, in either case, to any exemptive relief granted to us by the SEC (these provisions generally prohibit us from making additional borrowings, including through the issuance of additional debt or the sale of additional debt securities, unless our asset coverage, as defined in the 1940 Act, equals at least 200% after such borrowings); |

| • | pay dividends on, or purchase or redeem or make any payments in respect of, capital stock or other securities ranking junior in right of payment to the Notes, in each case other than dividends, purchases, redemptions or payments that would cause a violation of Section 18(a)(1)(B) as modified by Section 61(a)(1) of the 1940 Act or any successor provisions giving effect to (i) any exemptive relief granted to us by the SEC and (ii) no-action relief granted by the SEC to another BDC (or to us if we determine to seek such similar no-action or other relief) permitting the BDC to declare any cash dividend or distribution notwithstanding the prohibition contained in Section 18(a)(1)(B) as modified by Section 61(a)(1) of the 1940 Act in order to maintain the BDC’s status as a regulated investment company under Subchapter M of the Internal Revenue Code of 1986 (these provisions generally prohibit us from declaring any cash dividend or distribution upon any class of our capital stock, or purchasing any such capital stock if our asset coverage, as defined in the 1940 Act, is below 200% at the time of the declaration of the dividend or distribution or the purchase and after deducting the amount of such dividend, distribution or purchase); |

| • | sell assets (other than certain limited restrictions on our ability to consolidate, merge or sell all or substantially all of our assets); |

| • | enter into transactions with affiliates; |

| • | create liens (including liens on the shares of our subsidiaries) or enter into sale and leaseback transactions; |

| • | make investments; or |

| • | create restrictions on the payment of dividends or other amounts to us from our subsidiaries. |

In addition, the indenture will not require us to offer to purchase the Notes in connection with a change of control or any other event.

S-17

Furthermore, the terms of the indenture and the Notes do not protect holders of the Notes in the event that we experience changes (including significant adverse changes) in our financial condition, results of operations or credit ratings, as they do not require that we or our subsidiaries adhere to any financial tests or ratios or specified levels of net worth, revenues, income, cash flow, or liquidity.

Our ability to recapitalize, incur additional debt and take a number of other actions that are not limited by the terms of the Notes may have important consequences for you as a holder of the Notes, including making it more difficult for us to satisfy our obligations with respect to the Notes or negatively affecting the trading value of the Notes.

Certain of our current debt instruments include more protections for their holders than the indenture and the Notes. See “Risk Factors—In addition to regulatory requirements that restrict our ability to raise capital, our Credit Facilities, the Convertible Senior Notes and the 2019 Notes contain various covenants which, if not complied with, could accelerate repayment under the facility or require us to repurchase the Convertible Senior Notes and the 2019 Notes thereby materially and adversely affecting our liquidity, financial condition, results of operations and ability to pay dividends” in the accompanying prospectus. In addition, other debt we issue or incur in the future could contain more protections for its holders than the indenture and the Notes, including additional covenants and events of default. The issuance or incurrence of any such debt with incremental protections could affect the market for and trading levels and prices of the Notes.

An active trading market for the Notes may not develop or be maintained, which could limit the market price of the Notes or your ability to sell them.

The Notes are a new issue of debt securities for which there currently is no trading market. We intend to list the Notes on the NYSE within 30 days of the original issue date. Although we expect the Notes to be listed on the NYSE, we cannot provide any assurances that an active trading market will develop for the Notes or that you will be able to sell your Notes. If the Notes are traded after their initial issuance, they may trade at a discount from their initial offering price depending on prevailing interest rates, the market for similar securities, our credit ratings, general economic conditions, our financial condition, performance and prospects and other factors. The underwriters have advised us that they intend to make a market in the Notes, but they are not obligated to do so. The underwriters may discontinue any market-making in the Notes at any time at their sole discretion. Accordingly, we cannot assure you that a liquid trading market will develop for the Notes, that you will be able to sell your Notes at a particular time or that the price you receive when you sell will be favorable. To the extent an active trading market does not develop, the liquidity and trading price for the Notes may be harmed. Accordingly, you may be required to bear the financial risk of an investment in the Notes for an indefinite period of time.

If we Default on our obligations to pay our other indebtedness, we may not be able to make payments on the Notes.

Any default under the agreements governing our indebtedness, including a default under the Wells Facility, the Union Bank Facility, the Convertible Senior Notes, the 2019 Notes, and the Asset-Backed Notes or other indebtedness to which we may be a party that is not waived by the required lenders or holders, and the remedies sought by the holders of such indebtedness could make us unable to pay principal, premium, if any, and interest on the Notes and substantially decrease the market value of the Notes. If we are unable to generate sufficient cash flow and are otherwise unable to obtain funds necessary to meet required payments of principal, premium, if any, and interest on our indebtedness, or if we otherwise fail to comply with the various covenants, including financial and operating covenants, in the instruments governing our indebtedness, we could be in default under the terms of the agreements governing such indebtedness. In the event of such default, the holders of such indebtedness could elect to declare all the funds borrowed thereunder to be due and payable, together with accrued and unpaid interest, the lenders under the Wells Facility and the Union Bank Facility or other debt we may incur in the future could elect to terminate their commitments, cease making further loans and institute foreclosure proceedings

S-18

against our assets, and we could be forced into bankruptcy or liquidation. If our operating performance declines, we may in the future need to seek to obtain waivers from the required lenders under the Wells Facility or Union Bank Facility or the required holders of our Convertible Senior Notes, 2019 Notes, Asset-Backed Notes or other debt that we may incur in the future to avoid being in default. If we breach our covenants under the Wells Facility, Union Bank Facility, the Convertible Senior Notes, the 2019 Notes or other debt and seek a waiver, we may not be able to obtain a waiver from the required lenders or holders. If this occurs, we would be in default under the Wells Facility or Union Bank Facility, the Convertible Senior Notes, the 2019 Notes, the Asset-Backed Notes or other debt, the lenders or holders could exercise their rights as described above, and we could be forced into bankruptcy or liquidation. If we are unable to repay debt, lenders having secured obligations, including the lenders under the Wells Facility and the Union Bank Facility, could proceed against the collateral securing the debt. Because the Wells Facility, the Union Bank Facility and the Convertible Senior Notes have, and any future credit facilities will likely have, customary cross-default provisions, if the indebtedness under the Notes, the Wells Facility, Union Bank Facility, the Convertible Senior Notes, the 2019 Notes, or the Asset-Backed Notes or under any future credit facility is accelerated, we may be unable to repay or finance the amounts due. See “Description of the Notes.”

S-19

We estimate that the net proceeds we will receive from the sale of the $100.0 million aggregate principal amount of Notes in this offering will be approximately $96.5 million (or approximately $101.4 million if the underwriters fully exercise their overallotment option) after deducting the underwriting discount of approximately $3.0 million (or approximately $3.2 million if the underwriters fully exercise their overallotment option) payable by us and estimated offering expenses of approximately $500,000 payable by us.

We expect to use the net proceeds from this offering to fund investments in debt and equity securities in accordance with our investment objective and for other general corporate purposes. We may also use the net proceeds from this offering to fund the conversion of any of our Convertible Senior Notes which holders may elect to convert.

We intend to seek to invest the net proceeds received in this offering as promptly as practicable after receipt thereof consistent with our investment objective. We anticipate that substantially all of the net proceeds from any offering of our securities will be used as described above within three to six months, depending on market conditions. We anticipate that the remainder will be used for working capital and general corporate purposes, including potential payments or distributions to shareholders. Pending such use, we will invest a portion of the net proceeds of this offering in short-term investments, such as cash and cash equivalents, which we expect will earn yields substantially lower than the interest income that we anticipate receiving in respect of investments in accordance with our investment objective.

S-20

RATIO OF EARNINGS TO FIXED CHARGES

For the three month period ended March 31, 2014 and for the years ended December 31, 2013, 2012, 2011, 2010 and 2009, our ratio of earnings to fixed charges, computed as set forth below, were as follows:

| For the three months ended March 31, 2014 |

For the year ended December 31, 2013 |

For the year ended December 31, 2012 |

For the year ended December 31, 2011 |

For the year ended December 31, 2010 |

For the year ended December 31, 2009 |

|||||||||||||||||||

| Earnings to Fixed Charges(1) |

3.41 | 3.83 | 2.97 | 3.95 | 1.51 | 2.20 | ||||||||||||||||||

For purposes of computing the ratios of earnings to fixed charges, earnings represent net increase in stockholders’ equity resulting from operations plus fixed charges. Fixed charges include interest and credit facility fees expense and amortization of debt issuance costs.

| (1) | Earnings include net realized and unrealized gains or losses. Net realized and unrealized gains or losses can vary substantially from period to period. |

S-21

The following table sets forth (i) our actual capitalization as of March 31, 2014, and (ii) our capitalization as adjusted to give effect to the sale of $100.0 million aggregate principal amount of Notes in this offering (assuming no exercise of the overallotment option) after deducting the underwriting discounts and commissions of approximately $3.0 million payable by us and estimated offering expenses of approximately $500,000 payable by us. You should read this table together with the “Use of Proceeds” section and our statement of assets and liabilities included elsewhere in this prospectus supplement.

| As of March 31, 2014 | ||||||||

| Actual (in thousands) |

As

Adjusted (in thousands) |

|||||||

| Investments at fair value |

$ | 890,662 | $ | 890,662 | ||||

| Cash and cash equivalents |

$ | 224,538 | $ | 321,038 | ||||

| Debt: |

||||||||

| Wells Facility |

— | — | ||||||

| Union Bank Facility |

— | — | ||||||

| Accounts payable and accrued liabilities |

$ | 8,962 | 8,962 | |||||

| Long-term SBA debentures |

190,200 | 190,200 | ||||||

| Convertible Senior Notes |

72,789 | 72,789 | ||||||

| 2019 Notes |

170,364 | 170,364 | ||||||

| Asset-Backed Notes |

63,782 | 63,782 | ||||||

| Notes offered hereby |

— | 100,000 | ||||||

|

|

|

|

|

|||||

| Total debt |

$ | 506,097 | $ | 606,097 | ||||

| Stockholders’ equity: |

||||||||

| Common stock, par value $0.001 per share; 100,000,000 shares authorized; 61,760,434 shares issued and outstanding(1) |

$ | 62 | $ | 62 | ||||

| Capital in excess of par value |

656,869 | 656,869 | ||||||

| Unrealized appreciation (depreciation) on investments |

2,607 | 2,607 | ||||||

| Accumulated realized gains (losses) on investments |

(10,368 | ) | (10,368 | ) | ||||

| Undistributed net investment income |

4,132 | 4,132 | ||||||

|

|

|

|

|

|||||

| Total stockholders’ equity |

$ | 653,302 | $ | 653,302 | ||||

|

|

|

|

|

|||||

| Total capitalization |

$ | 1,159,399 | $ | 1,259,399 | ||||

|

|

|

|

|

|||||

(1) Does not include the 650,000 shares of our common stock issued under our ATM Program.

S-22

We are offering the Notes described in this prospectus supplement and the accompanying prospectus through a number of underwriters. Keefe, Bruyette & Woods, Inc., Jefferies LLC and RBC Capital Markets, LLC are acting as representatives of the underwriters. We have entered into an underwriting agreement with the underwriters. Subject to the terms and conditions of the underwriting agreement, we have agreed to sell to the underwriters, and each underwriter has severally and not jointly agreed to purchase from us, the aggregate principal amount of Notes listed next to its name in the following table:

| Underwriter | Principal Amount |

|||

| Keefe, Bruyette & Woods, Inc. |

$ | 26,000,000 | ||

| Jefferies LLC |

21,000,000 | |||

| RBC Capital Markets, LLC |

21,000,000 | |||

| BB&T Capital Markets, a division of BB&T Securities, LLC |

8,000,000 | |||

| Janney Montgomery Scott LLC |

12,000,000 | |||

| JMP Securities LLC |

4,000,000 | |||

| Sterne, Agee & Leach, Inc. |

8,000,000 | |||

|

|

|

|||

| Total |

$ | 100,000,000 | ||

Subject to the terms and conditions set forth in the underwriting agreement, the underwriters have agreed, severally and not jointly, to purchase all of the Notes sold under the underwriting agreement if any of these Notes are purchased. If an underwriter defaults, the underwriting agreement provides that the purchase commitments of the nondefaulting underwriters may be increased or the underwriting agreement may be terminated.

We have agreed to indemnify the several underwriters against certain liabilities, including liabilities under the Securities Act, or to contribute to payments the underwriters may be required to make in respect of those liabilities.

The underwriters are offering the Notes, subject to prior sale, when, as and if issued to and accepted by them, subject to approval of legal matters by their counsel, and other conditions contained in the underwriting agreement, such as the receipt by the underwriters of officer’s certificates and legal opinions. The underwriters reserve the right to withdraw, cancel or modify offers to the public and to reject orders in whole or in part.

Commissions and Discounts

An underwriting discount of 3.0% per Note will be paid by us. This underwriting discount will also apply to any Notes purchased pursuant to the overallotment option.

The following table shows the total underwriting discounts and commissions that we are to pay to the underwriters in connection with this offering. The information assumes either no exercise or full exercise by the underwriters of their overallotment option.

| Per Note | Without Option | With Option | ||||||||||

| Public offering price |

$ | 25.00 | $ | 100,000,000 | $ | 104,600,000 | ||||||

| Underwriting discount |

$ | 0.75 | $ | 3,000,000 | $ | 3,138,000 | ||||||

| Proceeds, before expenses, to us |

$ | 24.25 | $ | 97,000,000 | $ | 101,462,000 | ||||||

The underwriters propose to offer some of the Notes to the public at the public offering price set forth on the cover page of this prospectus supplement and some of the Notes to certain other Financial Industry Regulatory Authority (FINRA) members at the public offering price less a concession not in excess of 2.00% of the aggregate principal amount of the Notes. The underwriters may allow, and the dealers may reallow, a discount not in excess of 1.20% of the aggregate principal amount of the Notes. After the initial offering of the Notes to

S-23

the public, the public offering price and such concessions may be changed. No such change shall change the amount of proceeds to be received by us as set forth on the cover page of this prospectus supplement.

The expenses of the offering, not including the underwriting discount, are estimated at $500,000 and are payable by us.

Overallotment Option

We have granted an option to the underwriters to purchase up to an additional $4,600,000 aggregate principal amount of the Notes offered hereby at the public offering price within 30 days from the date of this prospectus supplement solely to cover any overallotments. If the underwriters exercise this option, each will be obligated, subject to conditions contained in the underwriting agreement, to purchase a number of additional Notes proportionate to that underwriter’s initial principal amount reflected in the above table.

No Sales of Similar Securities

We have agreed not to directly or indirectly sell, offer to sell, enter into any agreement to sell, or otherwise dispose of, any debt securities issued by the Company which are substantially similar to the Notes or securities convertible into such debt securities which are substantially similar to the Notes for a period of 30 days after the date of this prospectus supplement without first obtaining the written consent of the representatives. This consent may be given at any time without public notice.

Listing

The Notes are a new issue of securities with no established trading market. We intend to list the Notes on the NYSE. We expect trading in the Notes on the NYSE to begin within 30 days after the original issue date under the symbol “HTGX.” Currently there is no public market for the Notes.

We have been advised by the underwriters that they presently intend to make a market in the Notes after completion of the offering as permitted by applicable laws and regulations. The underwriters are not obligated, however, to make a market in the Notes and any such market-making may be discontinued at any time in the sole discretion of the underwriters without any notice. Accordingly, no assurance can be given as to the liquidity of, or development of a public trading market for, the Notes. If an active public trading market for the Notes does not develop, the market price and liquidity of the Notes may be adversely affected.

Price Stabilization, Short Positions

In connection with the offering, the underwriters may purchase and sell Notes in the open market. These transactions may include overallotment, covering transactions and stabilizing transactions. Overallotment involves sales of securities in excess of the aggregate principal amount of securities to be purchased by the underwriters in the offering, which creates a short position for the underwriters. Covering transactions involve purchases of the securities in the open market after the distribution has been completed in order to cover short positions. Stabilizing transactions consist of certain bids or purchases of securities made for the purpose of preventing or retarding a decline in the market price of the securities while the offering is in progress.

The underwriters also may impose a penalty bid. This occurs when a particular underwriter repays to the underwriters a portion of the underwriting discount received by it because the representatives have repurchased Notes sold by or for the account of such underwriter in stabilizing or short covering transactions.

Any of these activities may cause the price of the Notes to be higher than the price that otherwise would exist in the open market in the absence of such transactions. These transactions may be affected in the over-the-counter market or otherwise and, if commenced, may be discontinued at any time without any notice relating thereto.

S-24

Electronic Offer, Sale and Distribution of Notes

The underwriters may make prospectuses available in electronic (PDF) format. A prospectus in electronic (PDF) format may be made available on a web site maintained by the underwriters, and the underwriters may distribute such prospectuses electronically. The underwriters may allocate a limited principal amount of the Notes for sale to their online brokerage customers.

Other Relationships

The underwriters and their affiliates have provided in the past and may provide from time to time in the future in the ordinary course of their business certain commercial banking, financial advisory, investment banking and other services to Hercules or our portfolio companies for which they have received or will be entitled to receive separate fees. In particular, the underwriters or their affiliates may execute transactions with Hercules or on behalf of Hercules or any of our portfolio companies.

The underwriters or their affiliates may also trade in our securities, securities of our portfolio companies or other financial instruments related thereto for their own accounts or for the account of others and may extend loans or financing directly or through derivative transactions to us or any of our portfolio companies.

We may purchase securities of third parties from the underwriters or their affiliates after the offering. However, we have not entered into any agreement or arrangement regarding the acquisition of any such securities, and we may not purchase any such securities. We would only purchase any such securities if—among other things—we identified securities that satisfied our investment needs and completed our due diligence review of such securities.